Climate Risk is Already Impacting US Fixed Income Fundamentals

Population, property value and financial impairment are all correlated with climate risk, and climate change will only enhance this impact

As we’ve added clients of our climate risk and social impact data for US Fixed Income investors and stakeholders at a growing rate over the last 18 months, every new product navigates an adoption curve and common objections:

“Climate risk is already priced into the market”

“I’m good…all municipal bonds and agency securities are inherently ESG”

“If climate risk mattered, Miami would have defaulted already. There’s never been a climate-related default”

The list goes on but, at best, such viewpoints lack nuance. At worst, they’re abjectly false. In reverse order:

- as long ago as 1900, Galveston defaulted on bond payments after a major flood

- within just the state of Texas we can show massive within muni sector differences on climate risk, carbon transition risk and social impact, and the same applies for mortgage-backed securities from New York to California.

- the first statement is a curiosity, borne out of a belief system favored by the algo traders but lacking in substance and, ironically for such a quant-defined cohort, lacking in data. As the owners of the only comprehensive climate risk data set for the municipal bond universe we would like nothing more than for climate to be a driver of price and yield, but to describe the signal as “weak” is generous based on 10 year historical analysis. The fact that climate risk is not priced into the market means a bubble exists that climate change will inflate.

All that said, we can show the impact of climate risk on population, property value and financial impairment, three key pillars of municipal and mortgage-backed security health, all tied to a single, all-encompassing metric. Climate risk is chipping away at the very foundations of US Fixed Income, but only now has the data existed to see this growing weakness.

The risQ Score

Credible and actionable climate risk analysis requires back-testing versus historical outcomes as well as modeling for future climate change scenarios. For those that don’t live in the insurance world, actionability also dictates easy to interpret metrics, even if they’re underpinned by the same richness of data and analysis an insurer expects. The risQ Score is that singular 0–5 metric for the US Fixed Income ecosystem i) encompassing Property Value at Risk and GDP Impairment Risk as key inputs; ii) back-tested against historical losses for key perils including flooding, hurricane and wildfire; iii) conditioned for future climate change to enable forward-facing projections on a location-by-location basis; and iv) via loan-to-pool linking in MBS or obligor-to-issuer linking in municipal bonds, applicable and available for all the associated CUSIP universes.

We can dissect, drill-down and differentiate based on the asset types impacted and the perils imparting the damage for a given CUSIP, but the risQ Score can simply and clearly stand alone in delivering new insights about climate risk.

Higher Climate Risk = Lower Home Price Appreciation

Zillow Home Value Index data from 2012 to 2020 at county level provides a powerful US-wide data set for prevailing residential property prices. Numerous factors are known to cause variance in home values and need to be controlled for, requiring parallel data to first be ingested. After accounting for regional trends (using state as a control variable), urbanization (population density), and affluence (through risQ’s Social Impact Score), a clear, statistically significant relationship between the risQ Score and home price appreciation is clear. For each one-point risQ Score increase there is a corresponding property value change of -2.0% (with 95% confidence intervals of -2.7% and -1.3%). Furthermore, we can break the overall risQ Score into peril-based components and extract still greater insight on home price depreciation correlated to climate risk (with 95% confidence intervals in brackets):

- Flood risQ Score: -1.2% [-1.7%, -0.7%]

- Wildfire risQ Score: -0.8% [-1.4%, -0.3%]

- Hurricane risQ Score: -0.3% [-1.2%, 0.1%]

The bottom line: Increasing the risQ Score by one integer holding all else constant implies a -2% discount for home price appreciation, and a -10% impact across the full 0 to 5 scale.

Higher Flood Risk = Lower Population Growth

To analyze population change we drew upon American Community Survey data at census tract level from 2010 to 2019 and accounted for the same control factors used above: regional trends (state as a control variable), urbanization (population density), and affluence (through risQ’s Social Impact Score). Isolating down to the Flood risQ Score, given its applicability across the entirety of the US, each 0.25 increment shows increasing negative impact on population. In the output below the number of census tracts in each group is shown in labels, while the 95% confidence intervals for population change are shown as a grey band. In the census tracts with the highest risk, overall size of population is impaired by 6.5% over 10 years.

The bottom line: At Flood risQ Scores of 3.5 and above, flood risk is a high confidence driver for net population loss, and even at 2.5 is more likely than not to enhance population loss.

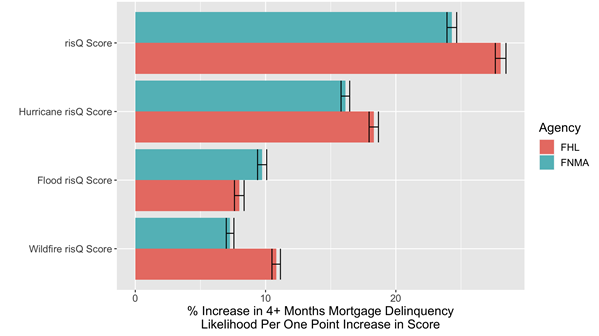

Higher Climate Risk = Higher Mortgage Delinquency

Using 27 million Fannie Mae and Freddie Mac loans originated from 2006 to 2018 and at Zip-3 level, the relationship between our 0–5 risQ Score and mortgage payment delinquency is clear. Given the timeframe cutting across the Global Financial Crisis, we controlled for macroeconomic factors, loan attributes, as well as state-level factors, and localized socioeconomics and evaluated whether loans experienced 4+ months of delinquency. As for the population data above, the number of loans in each group shown in labels and the 95% confidence intervals shown as a grey band. In this case, there is an increasing likelihood of delinquency from risQ Scores 2 and above; this trend accelerates and is statistically significant and outside of 95% confidence for risQ Scores of 3 and above. For loans with the highest risk, delinquency rates are 3 times higher than baseline rates.

As for home price appreciation above, there is also a peril-by-peril view that can be extracted, and also be viewed by agency given the differing loan locations profiles and programs prevalent across Fannie Mae and Freddie Mac. For each one point increase in risQ Score the odds of 4+ months of delinquency is 24% — 28%, while the peril-by-peril break-outs are:

- Flood risQ Score: 8% — 10%

- Wildfire risQ Score: 7% — 11%

- Hurricane risQ Score: 16% — 18%

The bottom line: Increasing the risQ Score by one integer holding all else constant implies ~ 25% increase in probability of 4+ months of loan delinquency, meaning it more than doubles across the full 0 to 5 risQ Score scale.

Is US Fixed Income Ready for Climate Change?

All of the above leverages historical data that should also serve as a wake-up call to the denialism and ESG platitudes that still exists across finite portions of the US Fixed Income ecosystem. It does not take a rocket surgeon to imagine how this climate risk toxin will grow with climate change. It will chip away at increasing rates at the financial foundation of population, property and payments that municipal bonds, mortgage-backed securities and all fixed income assets are built. We analyze all municipal bonds and all mortgage-backed securities for climate risk, social impact and, at the intersection of the two, climate justice. They all have their own unique character are most assuredly not created equal in this regard. Those differences are most assuredly not being accounted for in the markets today, with too many market participants either in denial or simply ignorant of the data that exists and the actions they can take. We have analyzed all the funds holding municipal bonds or US mortgage-backed securities using their most recent N-PORT filings, with one view from this tool shown below. In this case, the relative risQ Score of a given fund is shown on the x axis and Social Impact on the y axis. The color indicated the percentage of the fund that is directly credit exposed (municipal bonds, risk transfer MBS).

Even with a couple of funds are off scale to the right a wide range of climate risk exists across funds with high proportions of credit exposure. This further exemplifies how the climate risk, social impact and overall ESG profiles of these funds are very different. That is the obvious corollary of being comprised of CUSIPs that are very different.

The bottom bottom line: Climate risk matters for US Fixed Income. Climate risk is measurable for US Fixed Income. Climate change makes climate risk increasingly material for US Fixed Income

For more information on our analyses of municipal bonds and mortgage backed securities and fixed income funds analysis, please contact info@risq.io